Inherited IRAs have changed significantly — and the rules today require more active planning than ever.

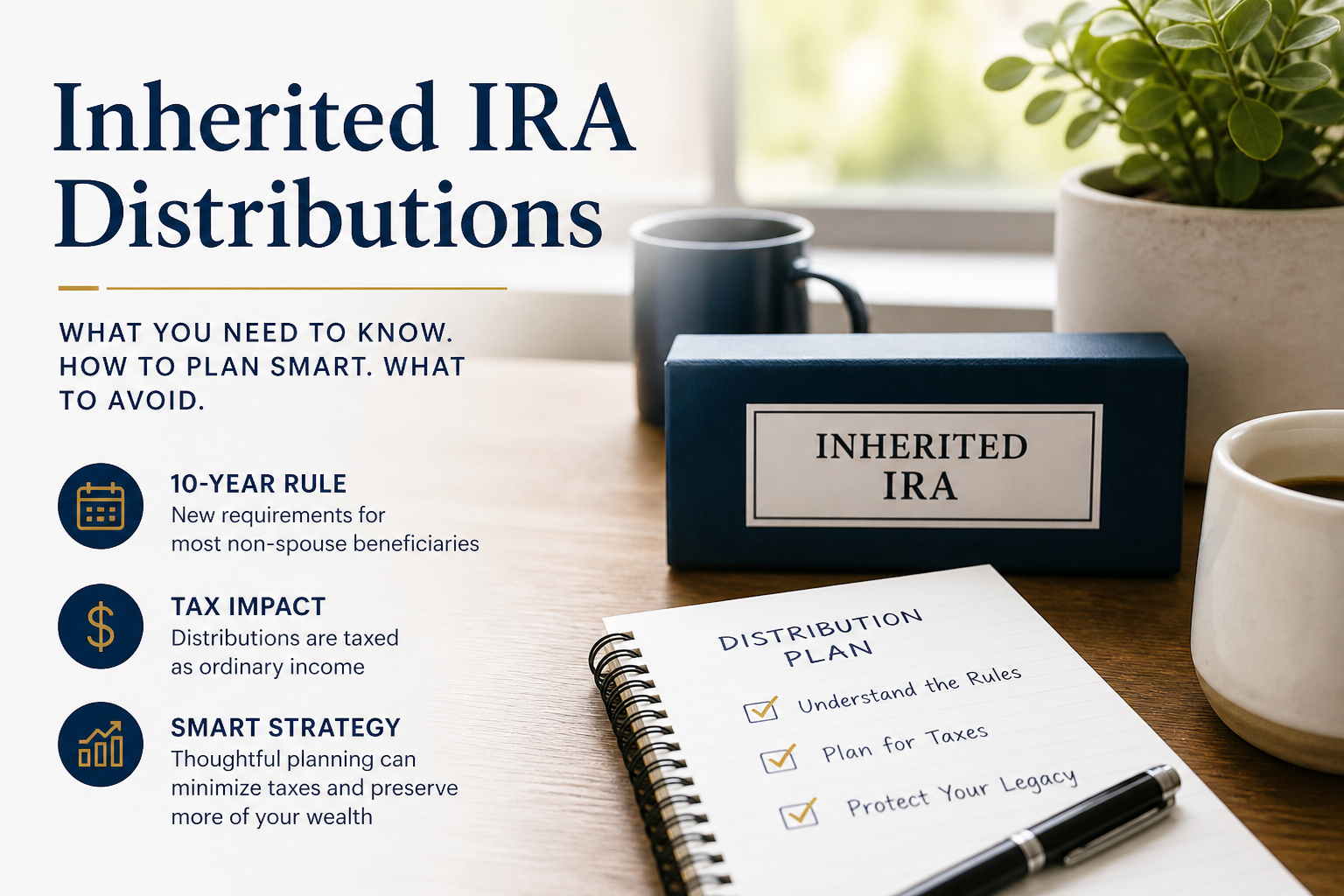

The 10-Year Rule

Most non-spouse beneficiaries must now withdraw the entire IRA within 10 years.

But there's an important distinction:

- If the original owner had already started RMDs → annual distributions are required during years 1–9

- If not → no annual requirement, but the account must still be emptied by year 10

Spouse vs. Non-Spouse Flexibility

Spouses have more options, including rolling the IRA into their own and delaying distributions.

Non-spouse beneficiaries generally must follow the 10-year rule with less flexibility.

The Tax Impact

Distributions from inherited traditional IRAs are taxed as ordinary income, which can:

- Push you into higher tax brackets

- Increase Medicare premiums

- Reduce tax efficiency if taken all at once

Smart Planning Matters

Even within these rules, strategy makes a difference:

- Spread distributions over time to manage tax brackets

- Align withdrawals with lower-income years

- Coordinate with your overall portfolio and tax plan

- For forward planning, consider Roth conversions to reduce the tax burden on heirs

Bottom Line

Inherited IRAs are no longer "set it and forget it."

A thoughtful distribution strategy can significantly improve after-tax outcomes — while poor timing can create unnecessary tax drag.